Up to 75% Subsidy: The Second Cycle of the “Large Investments” Scheme under Development Law 4887/2022 has been announced, with a total budget of €150 million.

Introduction

The “Large Investments” Scheme aims to support large-scale investment projects focused on key sectors of the Greek economy. Its objective is to substantially boost development and generate multiplier effects for local economies through the implementation of high value-added projects.

The total budget of the Scheme for 2026 amounts to €150.000.000, allocated as follows:

- €75.000.000 for tax exemption

This concerns investment projects opting for support through tax relief, providing significant incentives for reducing the investors’ tax burden.

- €75.000.000 for direct financial aid, which includes:

- Capital grants

- Leasing subsidies

- Subsidies for the cost of new employment

The direct aid is financed through the Public Investment Budget (PIB) of the Ministry of Development.

Eligible Beneficiaries & Participation Requirements

Beneficiaries of the aid provided under the “Large Investments” Scheme are investment project entities that:

- Have or are expected to acquire business activity within the Greek Territory at the time of commencement of works of their investment project.

- Operate or will operate under one of the following legal forms:

- Commercial companies (such as SA, Ltd, Private Company, General Partnership, Limited Partnership),

- Cooperatives,

- Special forms of cooperative entities, such as Social Cooperative Enterprises (Koin.S.Ep.), Agricultural Cooperatives (AC), Producer Groups (PG), Urban Cooperatives, Agricultural Corporate Partnerships (A.E.S.),

- Companies under merger, provided that the necessary publicity procedures have been completed prior to the commencement of investment works,

- Consortia engaged in commercial activity,

- Public and municipal enterprises, as well as their subsidiaries, under the following strict conditions:

- They have not undertaken the execution of a public service purpose,

- They have not been granted an exclusive state assignment for the provision of specific services,

- Their operation is not subsidised by public funds during the period of compliance with long-term obligations, in accordance with Article 25 of the law.

Non-Eligible Enterprises (Exclusions)

The following categories are explicitly excluded from participation in the Scheme:

- Enterprises subject to recovery procedures of state aid, pursuant to previous European Commission decisions (Deggendorf principle), at the time of application submission.

- Undertakings in difficulty, as defined in paragraph 18 of Article 2 of the General Block Exemption Regulation (GBER), assessed both at the level of the applicant company and at group level.

- Enterprises that have relocated, or refuse to commit not to relocate, the business establishment where the initial investment is to be implemented:

- if relocation occurred within two (2) years prior to the application submission, or

- if they refuse to commit that they will not transfer the establishment to another EU Member State for at least two (2) years after the completion of the investment.

- Enterprises implementing investment projects on behalf of the State, arising from works contracts, concession agreements, or service provision agreements.

- Enterprises subject to outstanding recovery orders at the time of submission of the investment application.

- Enterprises that have been sanctioned for violations of labour legislation (Article 40 of Law 4488/2017 (A’ 137), concerning exclusion of potential beneficiaries from aid schemes).

Types of Eligible Investment Projects

The supported investment schemes include:

- Establishment of a new production unit.

- Expansion of production capacity of an existing facility (unit).

- Diversification of an existing facility into new products or services that have never been produced or provided before, provided that eligible costs exceed at least 200% of the book value of reused assets, as recorded in the tax year prior to the application for inclusion.

- Fundamental change of the overall production process of an existing unit, where for large enterprises eligible investment costs must exceed the depreciation of the last three fiscal years of assets related to the activity being modernised. If such depreciation is not clearly recorded, the condition is considered not met. In addition, replacement investments and the acquisition of shares in another enterprise are not considered initial investments.

Core Participation Requirement for Potential Beneficiaries – Incentive Character

The state aid granted under the “Large Investments” Scheme is strictly of an incentive nature, in accordance with the applicable national and EU regulatory framework. Aid is granted exclusively for investment activities that would not be carried out in the absence of the incentive provided by the support scheme.

The fundamental requirement for preserving the incentive effect is the submission of a written application for inclusion in the Scheme prior to the commencement of any work related to the investment project.

Any commencement of works before the submission of the application:

- Leads automatically to the rejection of the application, or

- If an approval decision has already been issued, results in its revocation, regardless of the stage of implementation of the investment, and within the monitoring period provided after project completion.

Definition of “Commencement of Works”

According to the General Block Exemption Regulation (GBER, Article 2, point 23), “commencement of works” means:

- For construction investments:

The earlier of the following events: either the physical start of construction works related to the investment, or the first legally binding commitment to order equipment or undertake any other expenditure that renders the investment irreversible.

The following are not considered commencement of works:

- Purchase of land.

- Preparatory actions such as permitting procedures or feasibility studies.

- For acquisition investments:

Commencement of works is considered the date of acquisition of the assets directly linked to the acquired establishment.

Project Budget, Aid Intensity and Level of Support

Within the framework of this Scheme, investment projects are eligible provided that the total budget of eligible expenditures exceeds the amount of €15.000.000.

The amount of aid granted may not exceed €20.000.000, unless a lower ceiling applies pursuant to paragraph 1 of Article 4 of the General Block Exemption Regulation (GBER).

Total Aid per Beneficiary and Associated Enterprises:

- For a single enterprise, the ceiling is €20.000.000.

- For the total of cooperating or linked enterprises, the ceiling amounts to €50.000.000.

Within the framework of the aid scheme, specific restrictions apply regarding the time horizon and maximum aid amounts for each investment project. Initially, these restrictions apply to investment projects within a three-year period from the date of submission of the application for inclusion. This means that the total amount of aid received by an investor must comply with the established ceilings over a three-year period.

The aid amount taken into account is that approved by the inclusion decision. If the total amount of aid exceeds the established limits, the excess is proportionally reduced by type of aid and category of expenditure. An increase of up to 50% of the ceilings is permitted in cases where aid is granted in the form of tax exemption, i.e., exemption from income tax payment. However, this increase always applies subject to the general limits preventing any breach of the maximum thresholds.

In addition, for eligible expenditures outside regional aid, the maximum aid amount per investment project may not exceed €1.000.000. An exception applies to expenditures concerning Small and Medium-sized Enterprises (SMEs), for which the same limit applies specifically, ensuring clear funding boundaries.

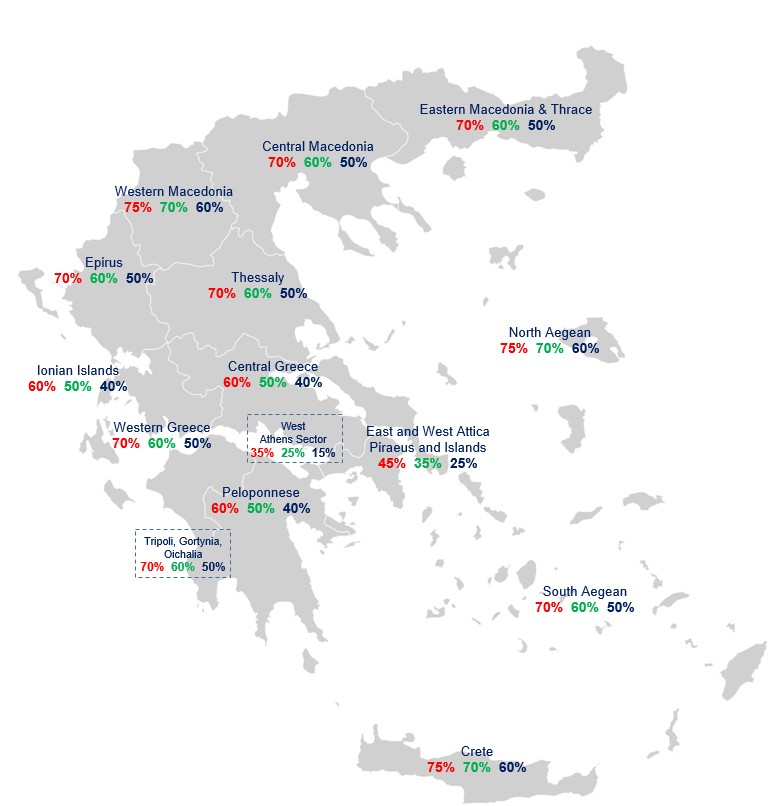

The aid intensities for eligible expenditures are determined based on the maximum limits set by the Regional Aid Map, as presented below.

Aid Intensities are determined based on the size of the enterprise and the region in which the investment is carried out. The basic distinction is structured as follows:

Maximum Aid per Investment Project:

The maximum amount of aid that can be granted per investment project does not exceed €20.000.000, unless stricter limits apply under the rules of the General Block Exemption Regulation (GBER).

Conditions and Restrictions:

- Increased intensities for SMEs do not apply to investment projects with eligible costs exceeding €50.000.000.

- In specific areas designated by the European Union, aid may be granted regardless of enterprise size for any initial investment.

- For large enterprises in restricted areas, aid is limited to new economic activities only.

- Very large investment projects (above €50.000.000) are subject to a degressive aid intensity system: 100% intensity for the first tranche of eligible costs up to €55.000.000, 50% for the tranche up to €110.000.000, and 0% beyond that level.

Types of Aid

For investment projects included under this Scheme, the following types of incentives are provided, designed to substantially support the development and sustainability of investments:

- Tax exemption: This provides exemption from income tax on pre-tax profits of the enterprise, in accordance with applicable tax legislation, excluding tax corresponding to distributed or withdrawn profits by partners. The amount of the exemption is calculated as a percentage of the value of the eligible investment expenditures or the value of new machinery and other equipment acquired through financial leasing (leasing). It is recorded as an equal reserve in a separate account in the financial statements.

- Grant: Direct financial support provided by the State to cover part of the eligible expenditures, calculated as a percentage thereof.

- Leasing subsidy: Coverage by the State of part of the instalments of a financial leasing agreement concluded for the acquisition of new machinery and other equipment. The subsidy is calculated as a percentage of the acquisition value, included in the lease payments, and lasts for up to seven (7) years, starting from the completion date of the investment.

- Subsidy of employment cost: Coverage by the State of part of the wage cost for new jobs created and linked to the investment project, provided that no other state aid is received for those positions.

Investment projects falling under specific aid schemes are excluded, namely those in the agri-food sector (primary production, processing of agricultural products and fisheries, Articles 65–71), tourism investments (Articles 84–90), and alternative forms of tourism (Articles 91–97) of Law 4887/2022.

Fast Licensing Incentive

Within the framework of the Scheme, a special fast-track licensing procedure is provided for investments that fall under the aid regime.

Following the submission of a complete application file by the investor to the General Directorate of Development Laws and Foreign Direct Investments, all required permits and approvals (including environmental and spatial planning authorisations) must be issued within two (2) months. If supporting information is missing, the administration may request additional data, effectively “suspending” the deadline until submission is completed.

The procedure is carried out with absolute priority. In the event that the deadline is exceeded, competence is transferred to the Minister of Development, who must issue a decision within one (1) month. The General Secretariat for Private Investments is also considered a competent licensing authority.

This fast-track licensing mechanism is designed to significantly reduce waiting times for permit issuance, limit administrative uncertainty, and strengthen investor confidence. It establishes a more predictable and investor-friendly administrative environment, with clear deadlines, institutional accountability, and defined intervention mechanisms in case of delays. The strategic objective is the immediate commencement of investment implementation without unjustified administrative bottlenecks, thereby enhancing the overall attractiveness of the country as an investment destination.

Main Categories of Eligible Expenditures

Eligible Expenditures for Regional Aid

The expenditures eligible for receiving regional aid within the framework of investment projects are defined as follows:

First, eligible expenditures include investments in tangible assets, which cover:

- Construction, expansion, and modernisation of buildings and auxiliary facilities. Special provision is made for constructions ensuring accessibility for persons with disabilities or reduced mobility, as well as for the landscaping of the surrounding area. However, such expenditures may not exceed 45% of the total eligible costs at the level of regional aid. It is noted that for certain activities, such as logistics services (code 2008 52.29.19.03 / code 2025 52.31.19.07), this percentage may reach 70%, while for investments in listed heritage buildings it may reach up to 80%. In addition, constructions legalised under the relevant provisions of Laws 1337/1983, 4178/2013, and 4495/2017 are eligible.

- Acquisition, for SMEs only, of part or all of existing fixed assets, such as buildings, machinery, and other equipment, subject to the following conditions: the enterprise has ceased operations; the acquisition is made from an unrelated party (except in the case of small enterprises acquired by employees or family members of the previous owner); and the transaction takes place under normal market conditions. It is important to note that fixed assets already subsidised under development laws or other schemes prior to acquisition are not eligible.

- Purchase and installation of new modern machinery and equipment, including technical installations and intra-unit transport vehicles.

- Leasing instalments for new machinery and equipment, provided that ownership is transferred to the lessee upon expiry of the lease agreement.

- Modernisation of specialised (non-building) installations and mechanical equipment.

Second, eligible expenditures include investments in intangible assets, which cover:

- Technology transfer through the acquisition of intellectual property rights, licences, patents, know-how, and unpatented technical knowledge.

- Quality assurance systems, certifications, as well as software procurement and installation and enterprise organisation systems.

To be eligible, the above expenditures must cumulatively meet the following conditions:

- be used exclusively within the funded business establishment,

- remain linked to the investment project for the duration of the long-term obligations,

- be depreciated in accordance with applicable accounting rules, and

- be acquired from independent third parties with no relation to the buyer.

- In addition, for large enterprises, eligible intangible assets are limited to a maximum of 30% of total eligible costs, while for SMEs the limit is 50%.

Third, eligible expenditures include wage costs for new jobs created as a result of the investment, calculated for two (2) years from the creation of each position. Wage cost is considered an eligible expenditure only on a standalone basis and not in combination with other investment costs.

Regarding wage costs, the following conditions apply: the investment must result in a net increase in employment, measured in Annual Work Units (AWU), at the business establishment compared to the average of the previous twelve months prior to the application. The positions must be filled within three (3) years from the completion of the investment, and each job must be maintained for at least five (5) years for large enterprises, four (4) years for medium-sized enterprises, and three (3) years for small enterprises.

Eligible Expenditures Outside Regional Aid

Within the framework of investment projects included in the present Scheme, there is the possibility of additional support beyond regional aid for specific categories of eligible expenditures, as defined in Article 6 of Law 4887/2022 and the General Block Exemption Regulation (GBER).

Eligible expenditures include the following categories:

- Advisory Services to Small and Medium-Sized Enterprises (SMEs): Eligible are studies and fees for external consultants related to investment projects of newly established SMEs (enterprises with less than 12 months of operating activity at the time of application submission). Routine operational consultancy costs, such as tax or legal services, are not covered.

- Energy Efficiency Measures: Eligible are additional investment costs aimed at achieving a higher level of energy efficiency, excluding measures in buildings governed by Article 38 of the GBER. Only investments exceeding applicable Union standards, or those implemented before such standards enter into force, are eligible.

- High-Efficiency Cogeneration of Energy from Renewable Energy Sources (RES): Investments in newly installed or renovated production capacity are subsidised, with aid intensity limits of up to 45% for renewable energy sources and up to 30% for other related investments.

- Installation of Efficient District Heating/Cooling Systems: Eligible are investment costs related to the construction or upgrading of energy-efficient systems, in accordance with Directive 2012/27/EU.

- Remediation of Environmental Damage and Restoration of Habitats: Eligible are costs related to remediation and restoration works, reduced by any increase in land or property value. Damage resulting from natural disasters or the cessation of industrial activity is not covered.

- Resource Efficiency and Circular Economy Support: Additional investment costs aimed at improving resource efficiency compared to less environmentally friendly alternatives are subsidised.

- Training of Employees: Eligible costs include trainers’ and trainees’ wages, operating expenses, materials, and consultancy services, aimed at upskilling or retraining personnel. Mandatory training required by law is excluded.

- Participation of SMEs in Trade Fairs: Eligible are costs related to rental, installation, and operation of exhibition stands at trade fairs.

- Employment of Disadvantaged and Disabled Workers: Eligible are wage costs for up to 12 months (or up to 24 months for particularly disadvantaged individuals), subject to conditions of net employment increase.

- Research and Development Projects: Eligible are personnel costs, materials, equipment, and other related expenses for basic research, industrial research, experimental development, and feasibility studies.

Non-Eligible Expenditures

- Operating Expenses: Costs related to the operation of the investment are not financed, such as payroll expenses, rent, utility bills, and other operational needs.

- Purchase of Furniture and Office Equipment: Financing of office furniture and equipment is excluded, unless these constitute an integral and necessary part of the production equipment of the investment.

- Purchase of Passenger Vehicles: The acquisition of passenger vehicles of up to six (6) seats is not considered an eligible expenditure.

- Purchase of Land, Plots, and Agricultural Land: Expenditures for the acquisition of land are not eligible for support. In cases involving the purchase of building facilities, the value of the land on which they are constructed is not covered.

- Contributions in Kind to Share Capital: Contributions to share capital in the form of real estate, machinery, or other fixed assets are not subsidised.

- Construction or Expansion of Buildings on Non-Owned Land: The construction or expansion of building facilities on land not owned by the investment entity is not eligible, unless:

- the land has been granted by the State or a public sector entity, or

- it has been legally leased from a public or private entity, with the lease duly registered or recorded in accordance with the procedures of the AADE (Independent Authority for Public Revenue) and the Cadastre, ensuring the right of use is maintained for at least the duration of the long-term obligations of the investment plus four (4) additional years.

Scoring Criteria

The scoring criteria of the “Manufacturing – Supply Chain” scheme (Law 4887/2022) are divided into four evaluated groups, as presented below:

Group A: Assessment of Project Maturity (score 0–45)

This group examines factors demonstrating the readiness of the investment for implementation, such as:

-

- Availability of the site for installation.

- Submission of applications for environmental licensing, building permits, amendment of building permits, or installation permits.

- Priority is given to organised business parks.

- Next in priority are designated areas that have not yet obtained full licensing.

- Finally, installations outside these areas receive a lower score.

Group B: Financial Assessment of the Beneficiary (score 0–25)

The evaluation differs depending on whether the beneficiary is an existing or a new entity:

- For existing entities, financial ratios are calculated based on the average values of financial data recorded in the financial statements of the last two (2) closed fiscal years prior to the submission of the application.

- For new entities, the assessment is based on the financial data of their shareholders/partners from the last two closed fiscal years, as follows:

- Shareholders/partners that are legal entities: If they hold more than 25% participation in the investment entity, the financial data of the companies in which they participate are taken into account on an aggregate basis for the last two years.

- Shareholders/partners that are natural persons with participation in other companies: If they hold more than 25% in the investment entity and more than 25% in other companies, the financial data of those companies are also included on an aggregated basis.

- Shareholders/partners that are natural persons exercising management functions: If they hold more than 25% in the investment entity and have not exceeded 25% participation in other companies, but have exercised executive management (e.g. CEO, Executive Chairman) in other companies for at least six months per year, then the financial data of those companies are also taken into account.

Group C: Sustainability Assessment (score 0–15)

This group is based on two main criteria:

- STEP Seal Index: Evaluates the existence of certifications related to environmental management, social responsibility, and sustainable development.

- Export Orientation Index: Calculated as the average export percentage of the enterprise over the last two closed fiscal years prior to submission. The higher the export share, the higher the score.

Group D: Employment Growth Assessment (score 0–15)

The score is based on the number of new dependent employment positions expected to be created by the investment project, in relation to the total eligible cost of the investment (calculated per thousand euros).

The more jobs created relative to the level of expenditure, the higher the score.

Submission Period, Submission Method and Investment Project Implementation Duration

The application period for the inclusion of investment projects under this Scheme begins on 17 April 2026 and ends on 30 June 2026. Applications are submitted through the Information System for Development Laws and are filed with the following competent authorities:

For all other investment projects, submission is made to the General Directorate of Development Laws and Foreign Direct Investments of the General Secretariat for Private Investments of the Ministry of Development.

For further information regarding the new “Large Investments” incentive scheme under the revised Development Law 4887/2022, as well as for planning your investment projects, you may contact us at +30 231 552 000, +30 210 958 0000, or via email at [email protected].